Frequently Asked Questions

How much hybrid income do I actually need for this to work?

There is no single number, but the goal is not to replace your full corporate salary. It is to take enough pressure off the portfolio that the withdrawal rate drops into a sustainable range, typically below 3.5% depending on your portfolio size and timeline. For most executives we work with, $50,000 to $150,000 in flexible hybrid income during the transition years is enough to change the math significantly. The specific amount depends on your lifestyle spending, your portfolio balance, your other income sources, and when Social Security and any deferred comp distributions begin. A coordinated model of all these inputs is what tells you your actual number, not a rule of thumb.

What counts as hybrid income in retirement planning?

Hybrid income includes any earned income you generate on your own terms after leaving full-time corporate work. Common forms include consulting agreements with one or two clients, fractional executive roles at a company where you bring strategic value, board or advisory seats with a retainer, speaking or writing if your expertise supports it, and investment or ownership stakes in businesses where you contribute meaningfully. The key is that the intensity and schedule are yours to control, not a full-time employer's. Subject to your specific tax situation, self-employment income from consulting or advisory work is generally subject to federal and state income tax and self-employment tax, so the income plan should be modeled with those obligations factored in.

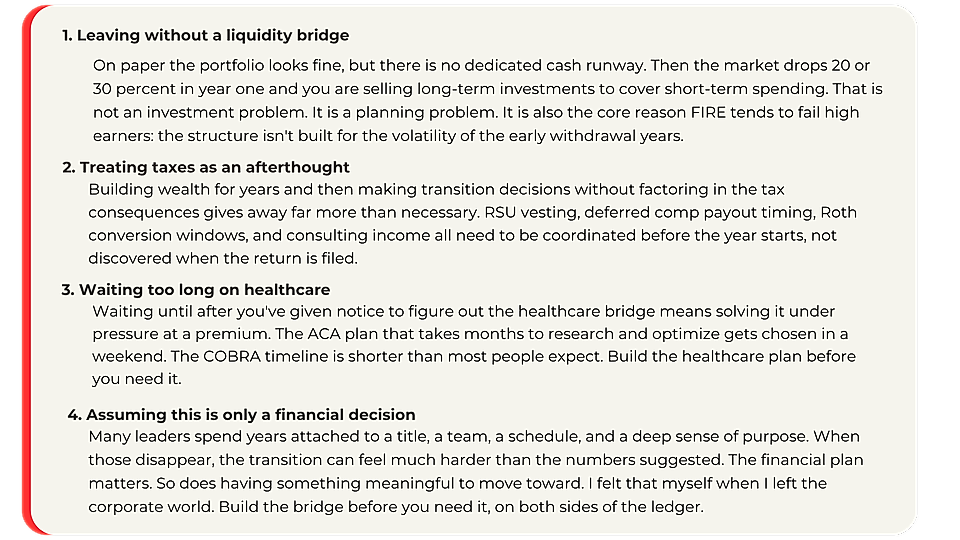

How do you handle healthcare between leaving corporate and Medicare at 65?

The healthcare bridge is one of the most important planning items before any transition and one of the most commonly underestimated costs. Options typically include COBRA continuation coverage for up to 18 months after leaving an employer, ACA marketplace plans where premium tax credits may be available if your income is managed carefully in the transition years, coverage through a spouse's employer plan if available, or a combination of these across different years. The right structure depends on your family situation, your health needs, your expected income level during the bridge years, and the specific plans available in your state. This needs to be modeled and decided before you give notice, not after.

What tax issues come up most often in the transition year?

The most common issue is income stacking: RSU vests, severance, deferred comp distributions, and consulting income all landing in the same tax year without coordination. This can push a high earner into peak marginal brackets in the exact year they were planning to benefit from lower income. The second most common issue is missing the Roth conversion window that opens up in the low-income years between leaving corporate and deferred comp or Social Security starting. If those years aren't modeled in advance, the window closes before it's used. Both issues are avoidable with multi-year planning. At Tailored Wealth, we model every significant income event across the transition years so nothing lands as a surprise.

How does Tailored Wealth help executives structure a hybrid retirement?

We build the full transition architecture as part of our Life-Driven Planning process: mapping the three-layer portfolio structure to your specific timeline, modeling hybrid income scenarios alongside your equity comp and deferred comp events, building the healthcare bridge before you leave, and running multi-year tax projections so the transition is coordinated rather than reactive. We use professional planning software to show you exactly what the numbers look like under different exit dates, income levels, and market scenarios. The Quarterly Strategy Rhythm keeps the plan current as your equity events, consulting income, and life circumstances evolve. The goal is a designed transition, not a hope-and-check approach.