TL;DR Answer Box

At $500K+ W-2 income, “maxed 401(k)” is not a strategy—it’s a starting line. High earners reduce tax drag by building infrastructure: (1) an entity that captures income you control outside your W-2 (and unlocks legitimate deductions and better tax treatment), and (2) stacked retirement “shelters” tied to that entity (often a Solo 401(k) and, when appropriate, a defined benefit plan). The goal isn’t gimmicks. It’s structure, documentation, and multi-year planning.

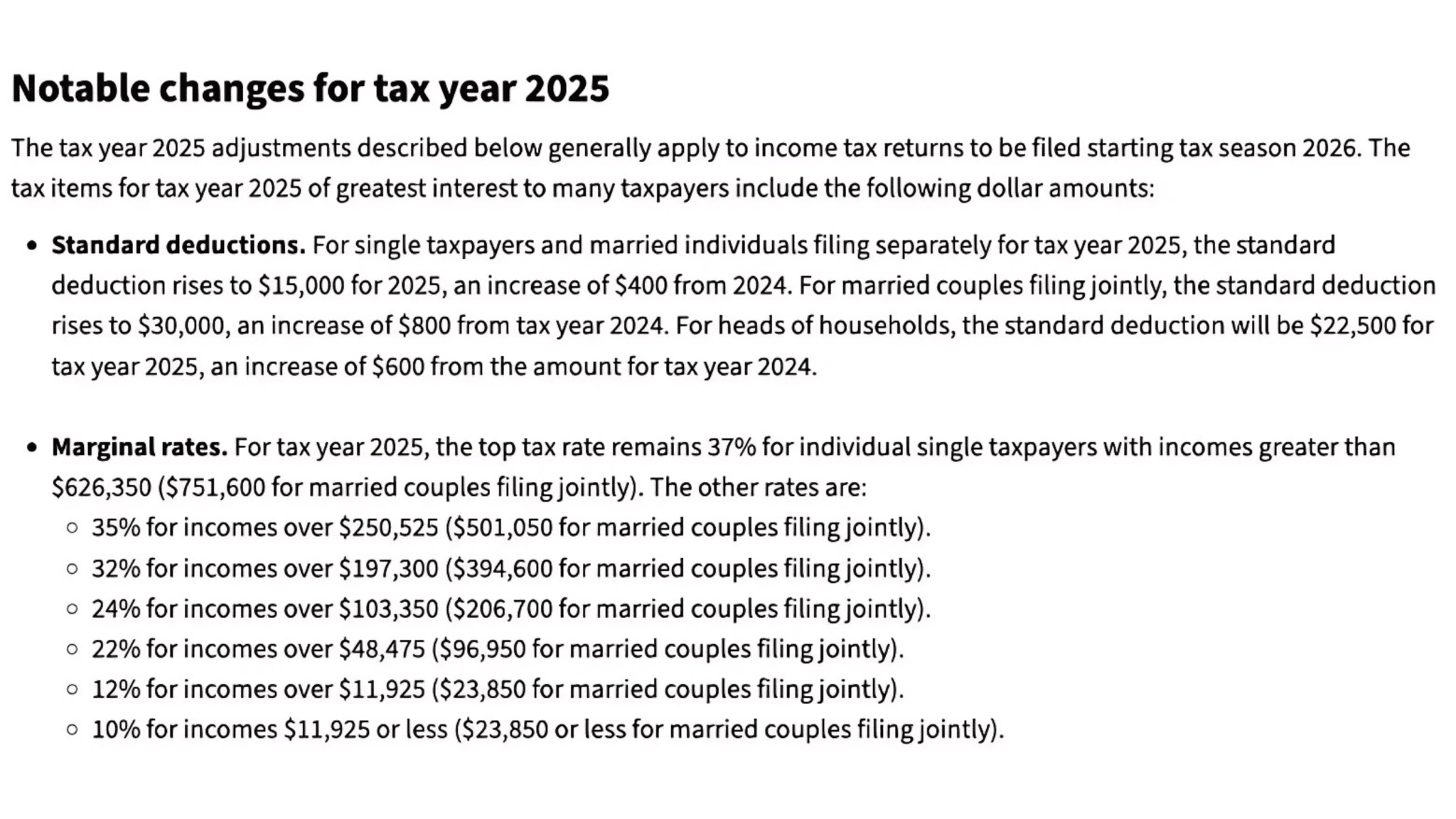

Last updated: January 28, 2026

At $500K+ W-2 income, normal rules stop applying. It can feel like you’re fighting less for gains and more to survive tax-wise.

High earners who thrive don’t just grind harder—they learn to play the system smarter. They build infrastructure, weaponize volatility, and steer every dollar with precision.

Today, we’re breaking down two elite moves, and why most top earners are still burning cash without realizing it.

🦾 Entity Engineering: Build Your Tax Machine

W-2 income is structurally rigid: full payroll withholding, limited deduction lanes, and very little flexibility around timing. That’s why many high earners build a separate “income engine” outside their employer—so at least some of their income runs through rules they can control.

Wall Street execs have had some version of this for decades. By creating a separate business entity (often with S-Corp taxation when it fits), you can gain control over how and when new income is received.

Let’s be dead clear:

- An LLC by itself does not lower your W-2 income or W-2 taxes.

- ✅ A side business set up properly can optimize taxes on business income you control.

- ❌ It does not change how your employer taxes your salary. That W-2 is locked in.

Why S-Corp taxation can matter (when it fits)

When you earn business income directly (sole prop / Schedule C), you generally pay self-employment tax on net profit (in addition to income tax), subject to rules and thresholds.

With S-Corp taxation, you typically pay payroll taxes on a reasonable salary, and remaining profit may be distributed as distributions (which can reduce exposure to certain payroll taxes compared to pure Schedule C treatment—fact dependent and must be structured correctly).

Important: the savings are not automatic. They come from:

- clean bookkeeping and documentation,

- reasonable salary support,

- legitimate deductions that match your business activity,

- and correct tax filing.

The “first steps” structure (simple version)

- Create a personal LLC (and evaluate whether S-Corp taxation makes sense).

- Define a reasonable salary if S-Corp taxation is elected.

- Track and substantiate qualified business deductions (ordinary and necessary, with receipts and a clean paper trail).

Advanced layering (not blanket prescriptions)

Then you can get more strategic—if your business model supports it and your tax/legal team signs off. Examples include:

- IP-holding company: Own trademarks, digital products, courses, or licensing assets and structure royalty/licensing flows appropriately.

- Family management company: A legitimate admin/services entity with real work, real invoices, and real documentation—useful for building systems and future scaling.

I share those last two points to get the creativity wheels spinning—not as an automatic recommendation. The rule is simple: substance first, structure second.

Video: High Earners — How a Side Hustle Can Slash Your Taxes and Build Wealth

🔥 Retirement Shelter XXL: Stack Deferrals the Right Way

Maxing out your employer 401(k) is a solid move—but for high earners, it’s often just the baseline. The “next level” is adding a second income source (business income) so you can unlock additional retirement shelters tied to that income.

The finesse: contribute more in monster income years, throttle back when earnings dip, and keep liquidity expectations realistic.

How the stacking can look (conceptual)

- Solo 401(k) / Individual 401(k): Contribution capacity depends on your business income, plan design, and annual IRS limits.

- Defined benefit / cash balance plan: Can allow very large deductible contributions (often six figures+), but requires actuarial design and ongoing funding discipline.

- 457(b) and other deferred comp lanes: Sometimes available through employers; separate rules apply and the details matter.

Watch out: defined benefit plans can feel like handcuffs if your cash flow isn’t stable. Once you start, the plan expects a funding rhythm. Set it up only when the business income is durable enough to support it.

Most players are stuck at “I think I maxed my 401(k).” Meanwhile, structured earners can be building far more tax-advantaged capacity—quietly—because their income is engineered to support it.

💼 W-2 Side Hustle in Practice

Now meet Alina, a CFO with a bloated W-2 and rising income from coaching and author royalties.

Before the strategy, she ran it through a Schedule C—messy, exposed, and overtaxed.

After restructuring, she:

- improved her ability to qualify for pass-through planning lanes (where applicable),

- cleaned up deductions with better documentation and entity separation,

- built a retirement “stack” that matched her income volatility (Solo 401(k) + long-term shelter planning, when appropriate),

- segmented her IP/royalties into a cleaner structure for liability and clarity (fact-dependent).

Same human, two legal tax profiles. One set of income gets retirement benefits. Another gets treated like royalty flow—each with its own planning lane.

🎯 Making Sense of Your W-2 Side Hustle Strategy

This is the meta-game.

The point isn’t just to save on taxes—it’s to strategically set your moves multiple years out so your money flows intelligently, even when chaos hits.

By engineering your income, reducing tax drag, and keeping optionality alive, you’ll surprise yourself with how much wealth you can protect.

At this level, end-of-year defense alone won’t cut it. Strategic infrastructure wins.

Key Takeaways

- LLCs don’t reduce W-2 taxes—but they can optimize new income you control.

- S-Corp taxation can reduce certain payroll-tax exposure when structured correctly (reasonable salary + clean documentation).

- Business income can unlock additional retirement shelters beyond your employer plan.

- Defined benefit plans can be powerful—but require commitment and stable cash flow.

- Structure + documentation beats “creative ideas” every time.

CTA

If you’re a high-earning W-2 professional with meaningful side income (or you’re building one), we can map the cleanest structure: entity setup, deduction lanes, retirement stacking, and a multi-year plan that stays compliant.

Disclaimer

This content is for educational purposes only and is not tax, legal, or investment advice. Entity structuring, retirement plans, and deduction strategies are highly fact-dependent and require professional guidance. Consult your CPA, attorney, and other advisors before implementing any strategy.